The post Maternity insurance appeared first on Sky Financial Planning.

]]>Why get a maternity plan?

Your shield plan only covers the mother and does not cover for the newborn. Typically, for newborn, insurance can only be purchase when after 14 days when the baby is born. A maternity plan helps to guarantee insurance coverage for the newborn. This is particularly important if your child is born with health conditions, which could lead to them being rejected for insurance plans in the future.

Key highlights of AXA HappyMummy:

- Mothers carrying more than 1 foetus

- Coverage from 13 weeks into pregnancy

- Death of expectant mother up to S$30,000

- 15 pregnancy complications with payouts up to S$30,000

- Daily hospital cash benefits if mother or child is hospitalised (for maximum 60 days) up to S$600 a day up to S$18,000

- Early delivery by Caesarean Section up to S$4,500

- Death of the newborn child up to S$30,000

- 26 congenital illness up to S30,000

- Developmental delay of the newborn child up to S$3,000

- A free First Year AXA Shield Plan B for the newborn child without underwriting

Do contact for more information, and I will try my best to assist.

The post Maternity insurance appeared first on Sky Financial Planning.

]]>The post Premium financing appeared first on Sky Financial Planning.

]]>Let me give a simple example of how it can make sense.

For example, using a 1 mil annuity policy, paying 280k upfront and financing 720k at interest rate of 1.2% pa.

Yearly benefits can be up to $42,000.

Interest cost per year works out to $8,640.

Nett benefit after interest is $33,360.

This works out to a simple yield of 11.9% base on capital outlay of 280k.

Yield can be maximised further with an efficient allocation of the 720k, which would otherwise been used to pay for the premium. This strategy can work in your favour if you do know how to exercise it.

There are caveats to premium financing though. The most important of which is, premium financing should only be a discussion when the prospects has the capacity to pay the premiums out-of-pocket but chooses not to. It should not be used to allow people to buy life insurance they cannot otherwise afford to own. Interest rate risk is also another factor to consider, as rates will vary. An increasing interest rate will increase cost of financing. Individual situation may differ. Do work with qualified financial planners to assist you in weighing the benefits vs the risk of premium financing.

The post Premium financing appeared first on Sky Financial Planning.

]]>The post Productivity Solutions Grant (PSG) for SMEs appeared first on Sky Financial Planning.

]]>As announced during the Supplementary Budget 2020, Productivity Solutions Grant (PSG) will be enhanced raising the maximum funding support level from 70% to 80%. The scope of generic solutions will also be expanded to help enterprises implement COVID-19 business continuity measures:

- Online collaboration tools

- Virtual meeting and telephony tools

- Queue management systems

- Temperature screening solutions

A highlight is that the scope includes Laptop-Bundled Remote Working Solutions now!

As of writing, there are few vendors that are pre-approved to provide the packages. Let me summarise so you dun have to spend that much time prowling around.

| Axiom | M1 | Rentalworks | Singtel | |

|---|---|---|---|---|

| Price | starting at $2,060.82 | starting at $1,891 | starting at $1,795.46 | starting at 1948.98 |

| Laptop | Microsoft Surface Laptop 3 | Basic Laptop Processor: Minimum Core i5 Memory: 8GB RAM Storage: 500GB SSD HDD or 1TB SATA HDD Display: 12” FHD IPS AG Operating System: Windows10 Pro Last known: Lenovo IdeaPad S340 | Laptop with Min Specs: Intel Core i5 Processor 8th/10th Gen 8GB RAM 512GB SSD Integrated Graphics 12” – 15.6” Display Windows 10 Pro | Laptop Processor: Minimum Core i5 Memory: Minimum 8GB Storage: Minimum 512 SSD Display: Minimum 13 inch Operating System: Windows 10 Pro 64 Currently Lenovo ThinkPad E14 Previously HP Probook G7 |

Each laptop have to be packaged with at least 1 Microsoft 365 Business Standard subscription for 1 year, which is reflected in the lowest price. This is nett, inclusive of GST as well. Laptop models are not guaranteed.

Each company is entitled to a maximum of 3, for consideration of grants. SMEs can apply for PSG if they meet the following criteria:

- Registered and operating in Singapore

- Purchase/lease/subscription of the IT solutions or equipment must be used in Singapore

- Have a minimum of 30% local shareholding; with Company’s Group annual sales turnover less than S$100 million, OR less than 200 employers (for selected solutions only)

Application process:

- Contact the vendors for quotation.

- Submit grant request at Business Grant Portal, using the quotation from your chosen vendor.

- Upon receiving your PSG approval, you may confirm the order with the vendor and make the arrangements for payment and delivery.

- Submit receipts in the Business Grant Portal to claim. Note that GST component is not claimable.

Do feel free to let me know if you have questions or any updates on the laptops offered.

The post Productivity Solutions Grant (PSG) for SMEs appeared first on Sky Financial Planning.

]]>The post Does your car insurance cover flood damage? appeared first on Sky Financial Planning.

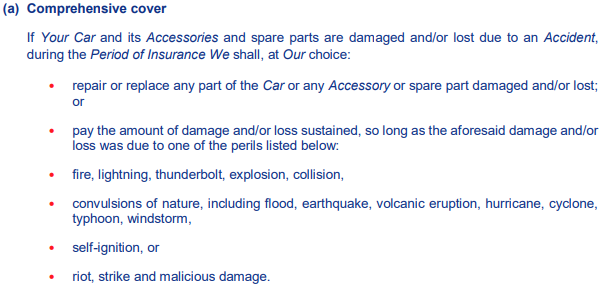

]]>I received a text from a concerned client asking if his car insurance covers for flood damages. My immediate thinking is whether his car is badly damaged. Thankfully, he asked out of curiosity.

Answer for this is subjective and highly dependent on the type of policy purchased. First and foremost, for AXA motor insurance, only comprehensive cover provides such coverage. Under comprehensive cover, there are plans such as Essential, Flexi, Peace, For Her, FlexiFamily, and more. The various plans have differing coverage and the choice depends on the needs of each car owner.

In summary, the policy he has does cover. With unexpected events happening, always prudent to work with your financial planner evaluate the risk you are exposed to. Does your car insurance policy cover?

The post Does your car insurance cover flood damage? appeared first on Sky Financial Planning.

]]>The post Cancer survivors appeared first on Sky Financial Planning.

]]>She wanted to get an insurance policy for her 17 year old sister. 4 years ago, her sister was diagnosed with medulloblastoma. Medical expenses became a heavy load. Fortunately, now her cancer is in remission, and do not require medical treatment for past 3 years.

As we all know, cancer patients or past cancer patients will not be able to get medical or critical illness coverage anymore. However, in the Singapore insurance market, there is an insurance policy exclusively for cancer survivors. This 22 year old girl was hopeful that she can get her sister covered, in the unfortunate case of relapse.

There are 3 main criteria,

- The applicant’s previous cancer can be of Carcinoma-in-situ (CIS) or Stages 1 to 3, except for brain cancer.

- The applicant has to be in remission for at least 3 years.

- The applicant has only 1 previous cancer.

Medulloblastoma is a type of brain cancer, rendering her sister ineligible for this.

Global medical insurance can cover pre existing condition, like this, but this is very costly. For reference, a 17 year old, it will cost SGD 12,000 + annually, which is unaffordable for the 22 year old university student.

Under such circumstances, I really felt helpless. All the policies covering life or critical illness require medical underwriting, which are unlikely to admit her sister.

In this age, where medical treatment gets more and more advanced, cancer is no longer a death sentence, but it still brings along a huge financial impact.

The above story is not a fiction. but a real life case, provoking a strong thought. Critical illness insurance can only be bought when healthy. That’s why we are always in a race to insure healthy lives before regrets set in. Nobody wishes for the unthinkable, but the truth is we cannot stop the unthinkable from happening, we can only reduce risk to the lowest. In this case, transferring economic/financial risk to the insurance company.

Readers who have any thoughts can feel free to contact. What I am racing for is less of sales results, more of no regrets…

The post Cancer survivors appeared first on Sky Financial Planning.

]]>The post Common questions on investment appeared first on Sky Financial Planning.

]]>The purpose of setting up this website is to share snippets which are easily understood. In the process, inspiring more people to take action. I wish to also apologise that I have not been updating as regularly as I wish to. I would also like to take this opportunity to thank the readers and people who write in. Your feedback are valued. Do feel free to email me, on your queries, and I will try my best to answer. Do also be assured that your confidentiality is respected.

Hope to write more in the coming weeks. Keep your questions coming in. Cheers.

The post Common questions on investment appeared first on Sky Financial Planning.

]]>The post AXA Wealth Treasure appeared first on Sky Financial Planning.

]]>- Enjoy an immediate boost to your investment with free bonus units of up to 100% in the first year.

- Get rewarded with loyalty bonus for staying longer, and achieve your investment goals faster.

- Flexibility in planning your investment portfolio with topup and withdrawal options.

- Access to diversified and exclusive funds through our platform.

- Facilitation of legacy planning

Want to find out more? Contact me for your personal consultation.

The post AXA Wealth Treasure appeared first on Sky Financial Planning.

]]>The post What to do when the market is trending up appeared first on Sky Financial Planning.

]]>So what can we learn from this. DJIA at trailing 12 months P/E of about 21 is not exactly cheap, yet the index still keep going up with little sign of slowing down. In the current environment, whether to load up and buy in depends on risk profile and appetite.

From a risk management perspective, I would exercise caution on entering large positions, and enter in tranches. This will allow me to enjoy the ride up if the market continues to trend upwards. If a market correction occurs, it will be an opportunity for me to accumulate more positions. With a plan in mind, I can sleep soundly every night despite the fluctuations in my investments portfolio.

Also, this brings back to the point of being in the market. I do not have a crystal ball, but generally, if I believe in the general growth of certain markets, it is ok to take a small position, and built upon it, while letting my wealth accumulate.

It all begins with a PLAN. “Fail to plan, or plan to fail”. It still boils down to PLANNING.

The post What to do when the market is trending up appeared first on Sky Financial Planning.

]]>The post 4 Reasons to be positive on Emerging Markets appeared first on Sky Financial Planning.

]]>4 reasons why I am positive,

- Attractive Valuation

With developed markets such as US running up to higher valuation, emerging markets equities at P/E ratio of 12 provide a comparatively more attractive valuation. - Stronger growth potential over developed markets

Economic growth is expected to rise with interest rates cut in a low interest rate environment. Coupled with an attractive valuation, it is likely to offer a higher capital gain. - Political reform

A huge risk in the emerging market space is usually political instability, which will hinder developments. Emerging economies are proactively implementing interest rates cut, or other policy easing measures, with an objective to spur growth. Notably, China, Russia, Turkey, and Indonesia are improving. India has also been cracking down on illegal money flow by removing the circulation of large denomination bank notes. There is a strong focus on infrastructure growth for India, and the country is also opening up for foreign direct investment. - Rising commodities prices

Oil price is stabilised above US$50 per barrel, and commodities market is also likely to be stabilising in 2017, reversing the bears in 2016. During the oil bear market, many policies were formulated to ease the impact on the economy. With the recovery of oil price, the policies still exist, and plays a pivotal role in adjusting the economies to the new equilibrium. Russia and Brazil are major producers that benefitted. Stabilisation of commodity prices has also helped reignite investors faith in emerging market with the improvement in the economic conditions in these countries.

Do feel free to contact me to exchange ideas. I am sure the investment journey is not easy, and it would be good to have another opinion as a reference.

Disclaimer: Views are strictly of my own, and do not constitute an offer to purchase. I am vested given that I believe in the growth story. Do exercise your due diligence.

The post 4 Reasons to be positive on Emerging Markets appeared first on Sky Financial Planning.

]]>The post Money not enough? You believe? appeared first on Sky Financial Planning.

]]>“I don’t come from a rich family.” – Duh, not many people have the privilege of being born wealthy. Warren Buffet, Jack Ma, they are not born into a rich family too. Many millionaires create their own success story, their own wealth, while you are dreaming of being endowed with it. Will your dreams come true if you do not take any actions?

“If I don’t work, how to survive, how to earn money? I got no time for other stuffs” – Yes, you need to work for money. How long can you trade your time for money? Why does the rich earn so much more than the regular people and have seemingly more time on hand? The rich knows that every one has the same 24 hours, make your time count, work smart, increase the value of their time. How can we reach there? Spend time building long term value, spend time building a stream of passive income. Achieve maximum impact with the same limited time everyone has.

“Investments, I don’t know how? Very dangerous.” – Not investing is even more dangerous, bleeding your hard earned money. Your purchasing power is going to decrease as the years and decades pass due to inflation. There are so much resources available to learn. There are people willing to share. Are you willing to absorb? Have you ever ace or even pass any exams by answering “Don’t know”?

“Don’t even have money how to plan my finances? I have a family to support, have so and so expenses….” – Not having enough money. How much is enough? So you think you do not have enough, and yet you believe you can cope with the rising cost of living, or sudden need for money due to unfortunate circumstances. Failure to plan is planning to fail. How to begin on your wealth accumulation if you do not bother in planning.

You can complain about anything and everything, money not enough. the economy. your job, destiny etc. If you do not believe in changing your current situation, it will remain as it is. Are these “reasons” really reasons or excuses? Any more you heard, do feel free to share with me.

The power of beliefs: It can limit or empower you. Choose to believe in changing your current situation, and your dreams will take shape. Choose not to, and continue letting your beliefs limit you, limit your potential and limit your quality of living.

If you do not manage money, money will manage you. Do not expect pity or mercy. Do you want to be a prisoner of money for the rest of your life, or do you want to be in control of your financial situation?

Your future is in your hands. You believe, you decide.

The post Money not enough? You believe? appeared first on Sky Financial Planning.

]]>